Synektik - Betting on Polish healthcare

Post is originally from my previous blog www.globalstockpicking.com

Summary

+ Strong core business of radiopharmaceuticals, natural moat where products can only be produced locally.

+ Added an extremely successful leg as exclusive Polish distributor of Da Vinci surgical systems. Sales have exploded on back of pent up demand for these systems.

+ Product for heart disease in pipeline, finalized Phase 2 trials, seeking Phase 3 partner. Similar product by US listed Lantheus brought 60m USD in milestone payments. Synektik MCAP is ~60m USD.

+ Strong Polish Macro backdrop with Europe's strongest GDP growth as tailwind for Poland to catch-up in terms of medical advancements.

- Covid-19 is as for most Pharmaceuticals hampering sales.

- There has already been some delays in finding a partner for the Phase 3 study.

Company Background

Synektik Group was established back in 2001 and started off servicing different types of medical equipment mainly for Siemens. Fairly early some IT solutions were also developed for archiving and distributing images as well as patient data admin. In 2004 a laboratory was established for medical imagine diagnostics. In 2010 the company acquired IASON and entered the field of radiopharmaceuticals. On this heritage of servicing equipment for large medical equipment companies and radiopharmaceuticals the company has grown together with the Polish economy and delivered strong revenue growth and product innovation.

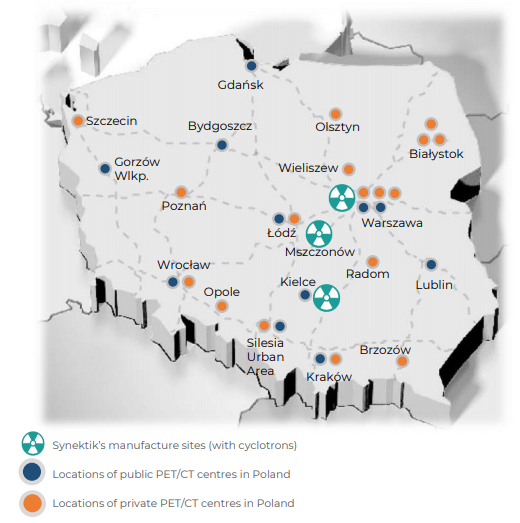

Today, Synektik is a leading Polish supplier of services and IT solutions for surgery, diagnostic imaging and nuclear medicine. Synektik operates a research laboratory for diagnostics imaging systems and a service center for medical equipment. The company is also the first commercial manufacturer of radiopharmaceuticals used in diagnostics for oncology (PET) in Poland. The Synektik Group operates three radiopharmaceutical manufacturing plants. Moreover, Synektik operates its own Research and Development Centre working on radioactive tracers for oncology, cardiology and neurology.

Management

The two largest shareholders are Mariusz Wojciech Książek, a Polish businessman (26%) who acquired his stake in the company late 2017 and the company CEO Cezary Kozanecki (25%).

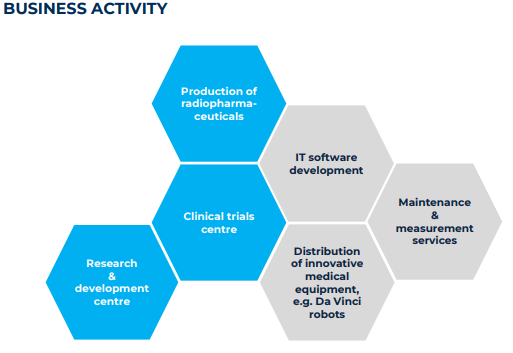

Business Segments

The company is standing on two main legs in terms of cash flow generation:

Radiopharmaceuticals

Distribution and service of medical equipment

The third important leg is the cardiotracer product where they are looking for a Phase 3 partner.

1. Nuclear medicine / Radiopharmaceuticals

Nuclear medicine is a medical speciality that uses targeted radioactive compounds, called radiopharmaceuticals, to diagnose, stage, treat and monitor diseases. Nuclear medicine can be divided into two categories: diagnostic nuclear medicine (or molecular imaging) and therapeutic nuclear medicine (or theranostics). The nuclear medicine market is predicted to reach $30 billion by 2030 worldwide.

Positron-emission tomography (PET) is a special form of medical imaging which enables doctors to visualize specific function inside the body in 3D. This is done with the use of a radiopharmaceutical, which is a special molecule combined with very small amount of radioactivity, and a special scanner. The images obtained can provide physicians with information to help them to diagnose, monitor and treat disease. The most frequently used PET imaging radiotracer is fluorodeoxyglucose (18F) (FDG), a compound made from a simple sugar and a small amount of radioactive fluorine (18F). This radiotracer accumulates in the body’s tissues and organs where there are increased levels of activity, such as in tumors. FDG is used in cancer imaging to search for tumors, metastases or to monitor response to certain therapies. However, it does not work well in some anatomical areas such as the prostate and the brain.

Synektik group produces a number of these basic radiopharmaceuticals and some special radiotracers. One example of a special radiotracer is produced under an agreement with Blue Earth Diagnostics. Fluciclovine (18F), a compound that is formed from a synthetic amino acid and includes a small amount of the radioisotope fluorine (18F). Fluciclovine (18F) accumulates in the body’s tissues and organs where there is an increased uptake of amino acids, as can occur in certain tumors. A PET/CT scanner is used to detect the distribution of the fluciclovine (18F). The images obtained from the fluciclovine (18F) PET scan give doctors information which can assist in the management of the patient. Fluciclovine (18F) is approved in the USA and Europe for PET imaging of biochemically recurrent prostate cancer.

The key point to understand with radiotracers are that they have to be produced locally. The whole idea of the compound is to have a very short half-life or radioactivity, to harm the patient as little as possible. So the product is made in a nearby cyclotrone the same morning. This creates a wide moat for the product, since a production facility in another country is too far away. There are 4 public cyclotrons, but they don’t have the license, they can only produce for their own hospitals. On top of that, Synektik is the only Polish company that can produce special radiopharmaceuticals, which translates to a 30-35% EBITDA margin. From this base of stable cashflow Synektik has been able to build up and scale its operations, organically and through acquisitions.

PET Tracer sector is hot

In recent years larges players have been snapping up assets in this space. Blue Earth Diagnostics that Synektik co-operates with was acquired by Bracco for 475m USD: Link

Novartis invested $6 billion to acquire Endocyte to expand expertise in radiopharmaceuticals: Link

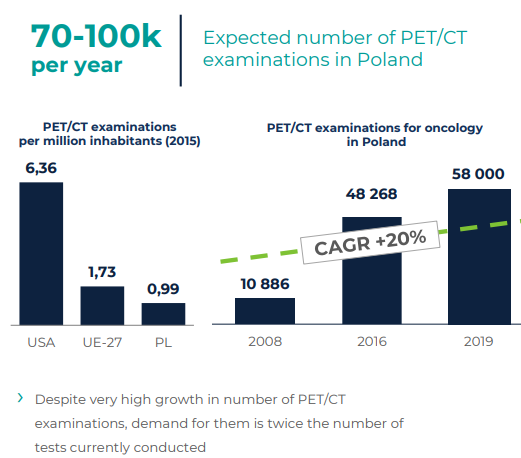

This is from a global perspective, as interesting to Synektik is how the market has developed locally in Poland. As you can see below there is plenty of room for growth.

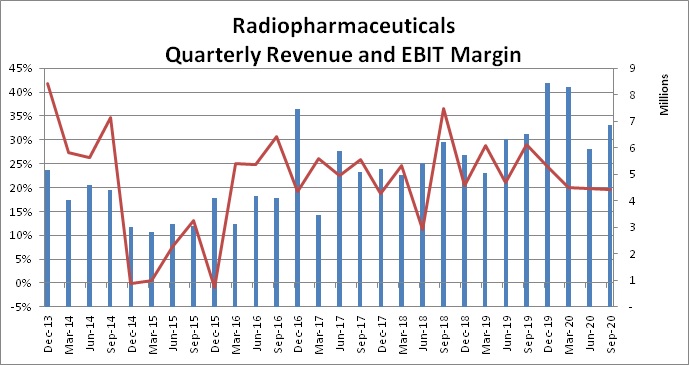

This is also translated into stable sales for Synektik with very stable EBIT margins:

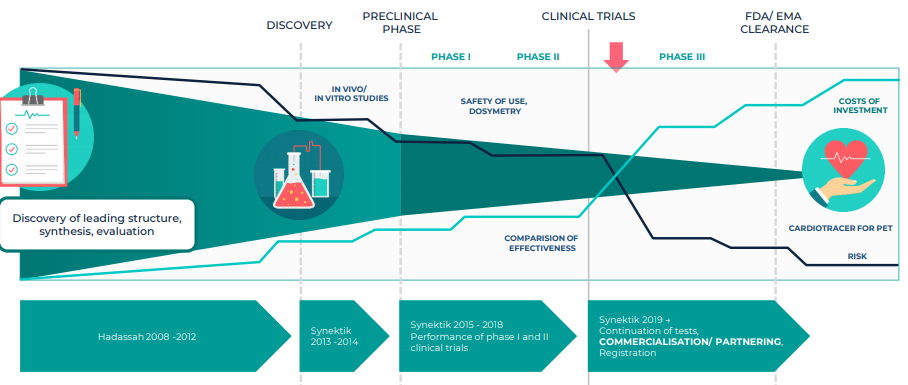

Cardiotracer - the gamechanger

What is most hot in this sector is of course not old technology that has been around for years, but new innovative tracers. Synektik has for a number of years been working on an improved tracer formula for heart disease. This project has been sponsored by EU Getting to the heart of diagnosis for imminent coronary artery disease.

The benefits of this new type of tracer is summarized by the following points:

high quality of image, strong sensitivity and adaptivity of the scan.

the same image quality for small and large patients, people with breast implants and those unable to lift up their hands.

four times less radiation (of significance to children and people with chronic coronary heart disease).

faster imaging protocols, leading to shorter test times

This cardiotracer product is Synektik's major research pipeline item and is a potential gamechanger for the company. The company has finalized Phase 1/2 studies and is now seeking a partner to take the product through stage 3 and to the market. Synektik have been dragging their feet a bit on finding a partner which has disappointed some investors.

Some comments around this topic from a recent investor chat with Synektik management:

We assume that 2021 will be the optimal time for concluding a contract with a partner. Of course, we DO NOT judge that it will happen. Why the frequent changes in schedules and delays in this area. I would like to ask for a more detailed explanation of this problem, as you have already failed to meet your declared deadline several times. You are talking about 2021 now, but you DON'T SEE it. So it may be later or not at all. This is very disturbing Dariusz Korecki: We would like to emphasize - we believe that concluding a contract next year would be optimal. But we are not going to make a deal at any cost under time pressure. Kardiagnnik is a one-of-a-kind project, and we will conclude a partnering contract for it only once. I assume that we all want this to be the best possible deal that will allow Synektik to become a global player. The game is at stake for our company. It would also be irresponsible on our part to ignore the impact of COVID on the course of the project in our plans.

The market speculates that the partner with whom the company will complete the third phase of clinical trials of the cardiac marker will be Astra Zeneca or Blue Earth. Can the company relate to these speculations? Dariusz Korecki: We cannot, by nature, comment on such speculations. In terms of direction, our partners may include drug manufacturers, manufacturers of medical equipment, who are also the largest producers of radiopharmaceuticals in the world. At this stage, we can reveal that we are in dialogue with the leading players in the global medical industry.

Do you have knowledge of the work on competitive markers for the tested cardiac marker? Cezary Kozanecki: We monitor the market, we have the fullest possible and current knowledge about it. The potential sales market is very large and competition is invariably limited.

Dariusz in the investor chat also points to Lantheus Medical one of few listed players in this space which made a deal with GE Healtcare, which provided for an upfront fee and success fee of approximately USD 60 million. This payment with potential good royalties for Lantheus was for more or less the same type of product: Phase III development and worldwide commercialization of flurpiridaz F 18, an investigational positron emission tomography (PET) myocardial perfusion imaging (MPI) agent that may improve the diagnosis of coronary artery disease (CAD), the most common form of heart disease. Link to press release.

Just to be clear, up-front and milestone payment during Phase 3 to Lantheus is 60m USD, which translates into 223m PLN and current MCAP of Synektik is 232m PLN. This 60m USD does not include future royalties if the product is launched. Synektik does not even need to land a deal half as good as Lantheus and this would still be massively accreditive to share price of Synektik.

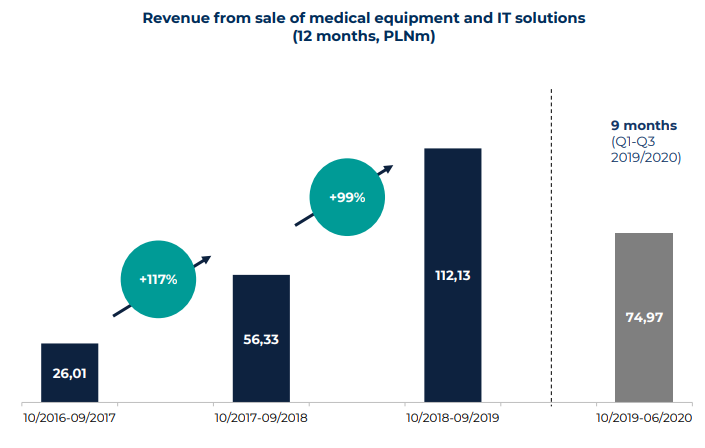

2. Distribution and service of medical equipment

Synektik has a number of products they distribute and do maintenance on in Poland. But the main driver of this sales is from the Da Vinci surgical machines.

Synektik is the exclusive distributor of da Vinci robotic systems in Poland. Under the agreement concluded with Intuitive Surgical, Synektik is responsible, for the sale and service of robots, instruments and equipment accessories, as well as training of operator doctors. Selling these machines gives firstly a nice one off cashflow (profit sharing with IS) but long term more importantly it builds up a base of service income of the surgery systems. Although Covid-19 has been very bad in Poland, Synektik has still managed to land a few sales during 2020:

November 2, 2020 the Company concluded an agreement with Międzyleski Szpital Specjalistyczny in Warsaw (Hospital). The contract was concluded as a result of the public procurement procedure conducted under the open tender procedure for the total net value of PLN 9,050,885. The system will be delivered by November 30, 2020.

April 21, 2020 the Company signed an agreement between the Company and the Independent Public Clinical Hospital No. 2 PUM in Szczecin. The contract was concluded as a result of the public procurement procedure conducted under the open tender procedure. Its value is PLN 12,496,500 net.

As you can see the agreement with Intuitive Surgical in July 2018 has been a game changer for this segment. My expectation is that sales of Da Vinci systems will increase further again after the pandemic. Synektik has made the estimate that approximately 40 Da Vinci systems will deployed in Poland until 2025. And very importantly create a new steady stream of service income. Synektik estimates by 2025 that service revenue will be more than yearly sales of Da Vinci systems (4 in past year and 5 estimated for 2021).

Other products

There are also other products where Synektik co-operates with various companies to access the Polish market. For example ZAP-X a new innovative system for stereotactic radiosurgery (SRS). The company has also continued to develop its IT platform for storing images. Called Zbadani.pl the company has ambitions to expand the platform to more centers with a wider set of functionality.

Another example is that Synektik obtained exclusivity in Poland for the distribution of Genomtec's two-gene tests (Genomtec® SARS-CoV-2 EvaGreen® RT-LAMP CE-IVD Duo Kit) for the diagnosis of SARS-CoV-2 infection.

Valuation

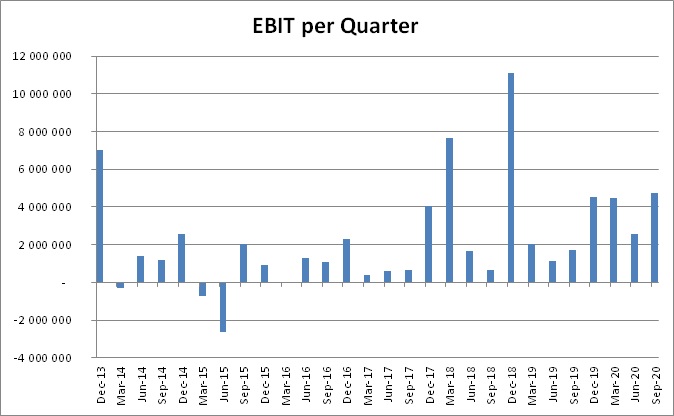

Although some larger Da Vinci sales in past years makes the EBIT quarterly data a bit lumpy, it's clear from the above picture that Synektik has established a new higher level of EBIT. And this is during Covid-19 when hospitals and the country is in partial lockdown. With Covid (hopefully) gone in 2022, I see possibilities for a very bullish growth scenario.

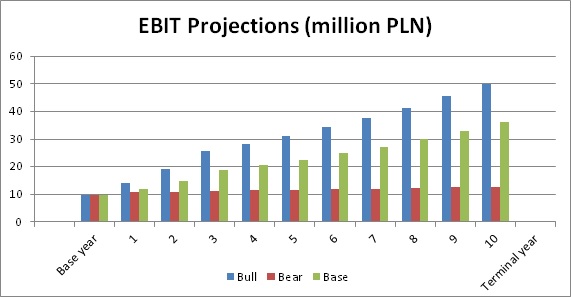

With a discount rate of 9% (Stable industry in Emerging Market) this gives me the following range of valuations:

Bull Case: 49 PLN per share - Assigned 30% probability

Bear Case: 14.6 PLN per share - Assigned 10% probability

Base Case: 35.5 PLN per share - Assigned 60% probability

Gives a weighted target price of 37.5 PLN per share versus its current price of 27.3 PLN. A decent 37% upside, but perhaps nothing to write home about. For the ones of you who read my post from top to bottom you know what I will say know. This does not account for the value for the cardio tracer product. Given that the company seems to have struggled somewhat to find the right partner I will be conservative and assign a third of the value of what Lantheus would get from only milestone payments. That is another 20m USD in pipeline value which translates into 8.8 PLN per share.

So my target price for Synektik with a conservatives pipeline valuation is 46 PLN per share or 68% upside to current share price.

If the company continues to execute as well as the past years and with a partner found in 2021 on good terms, I see much more upside than this over the coming 2-3 years.

Key metrics to follow in the future

Margin development - Valuation is fairly sensitive to changes in margin

Continued sales of Da Vinci machines and that nothing happens to the sales agreement (which currently lasts to 2022)

Further growth of radiopharmaceuticals expected, confirm that trajectory is intact

Partnering for Phase 3 of cardiotracer.

would you like to write a new update? what about valuation now?