Modern Dental (3600 HK) - follow up

Thoughts on the company and bull / bear arguments

Disclaimer: Healthy Stock Picks uses information sources believed to be reliable, but their accuracy cannot be guaranteed. The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. You are advised to discuss your investment options with your financial advisers and to understand whether any investment is suitable for your specific needs. From time to time, I may have positions in the securities covered in the articles on this website. Full disclosure: I do hold a position in Modern Dental Group when publishing this article. Note that this is a disclosure and not a recommendation to buy or sell.

In this note, I review what happened in Modern Dental since I published my write-up in April last year. I then address the main concerns that investors considering investing in the stock have.

I went to a new dentist last week, and as usual, I tried to chat about everything dental investment-related with my dentist. The comments from my dentist nicely tie into other discussions I had with investors interested in Modern Dental Group (MDG) the past months. One of those was a 45 min call with a European based fund manager that wanted to discuss the threats to MDG’s business model, so I thought I’d also share these thoughts here.

But first, a quick recap what happened company-wise since I published my write-up on the company back in April last year.

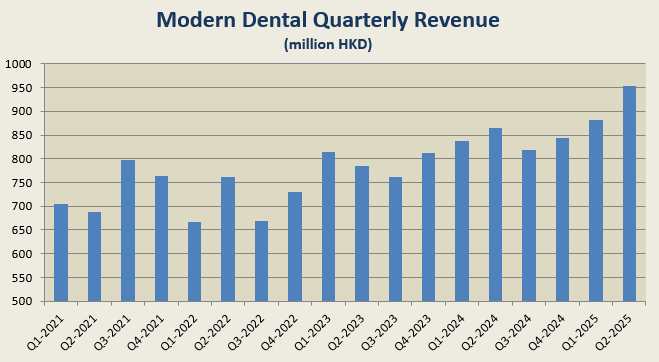

Revenue numbers

As Hong Kong has semi-annual reporting, not all numbers are available on a quarterly basis, but MDG does, on a voluntary basis, release some quarterly data. After the volatile Covid period, MDG has come out as a stronger company with a nice upward trend in revenue:

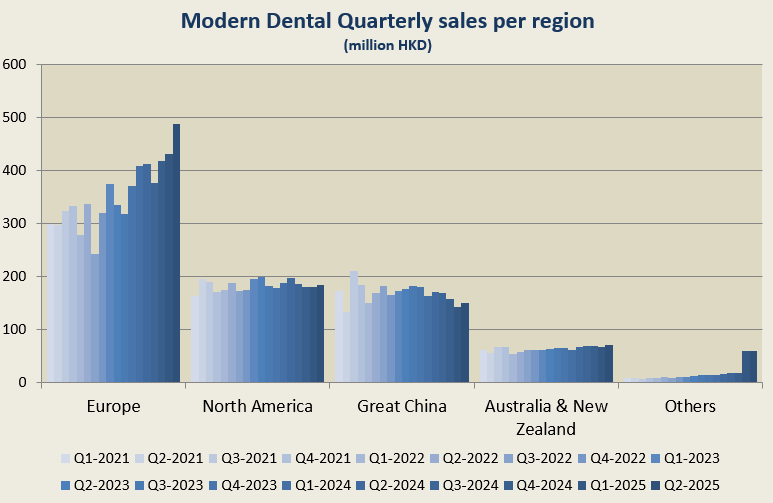

Below is my favorite chart to keep track of MDG:

As we can see the European region is really on fire, whereas North America continues to disappoint, and Great China (with a lot of Hong Kong exposure) is even declining. From a low level, AU/NZ is growing nicely and Others growth is related to the acquisition of Thai dental lab Hexa ceram, more on that later.

Concluding, revenue growth looks solid, but under the hood, it’s created quite unequally. How about profits? One of my main arguments in April 2024 was that the increased usage of digital intraoral scanners would lift margins. Has this happened? Yes but perhaps not only due to intraoral scanners.

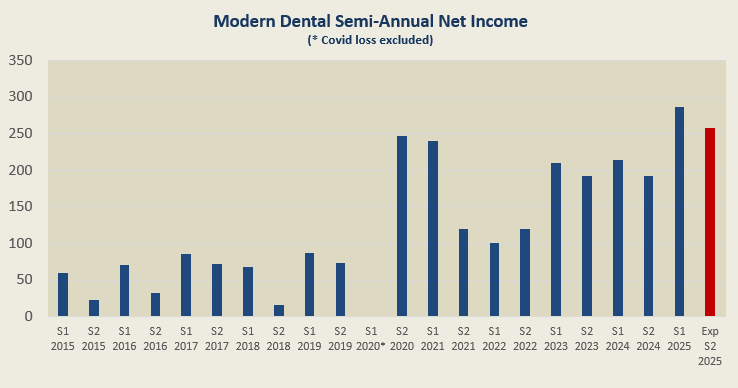

Profit

As we can see, the lift-off did not come immediately in 2024 when I did my write-up, but we had to wait until the first half 2025 profits for lift-off. The red bar is based on Bloomberg estimates for the second half profits, my own estimates are even higher.

And the stock price?

With Hang Seng ripping in Sep 2024, ironically Modern Dental did the opposite and visited the lows around HK$3.5. Then proceeded to tread water until the recent blow-out results were released. But overall, Modern Dental is still far behind the Hang Send Index since April 2024. I would argue though, that HSI is not a good benchmark for MDG, which is mostly a European business by now. I initially presented this stock idea on my old blog in Dec 2018. The stock chart looks slightly better when we zoom out a 22% 7 year CAGR:

Hexa Ceram purchase

Finally, to catch up to the present time, one has to mention the Hexa Ceram Thai dental lab purchase. To me this was big news as it had a solid impact on revenue growth and profits for 2025. Again ironically, the HK market is sometimes very inefficient, the acquisition was announced in Nov 2024 and the stock barely traded up on the news. For me this was extremely positive, why?

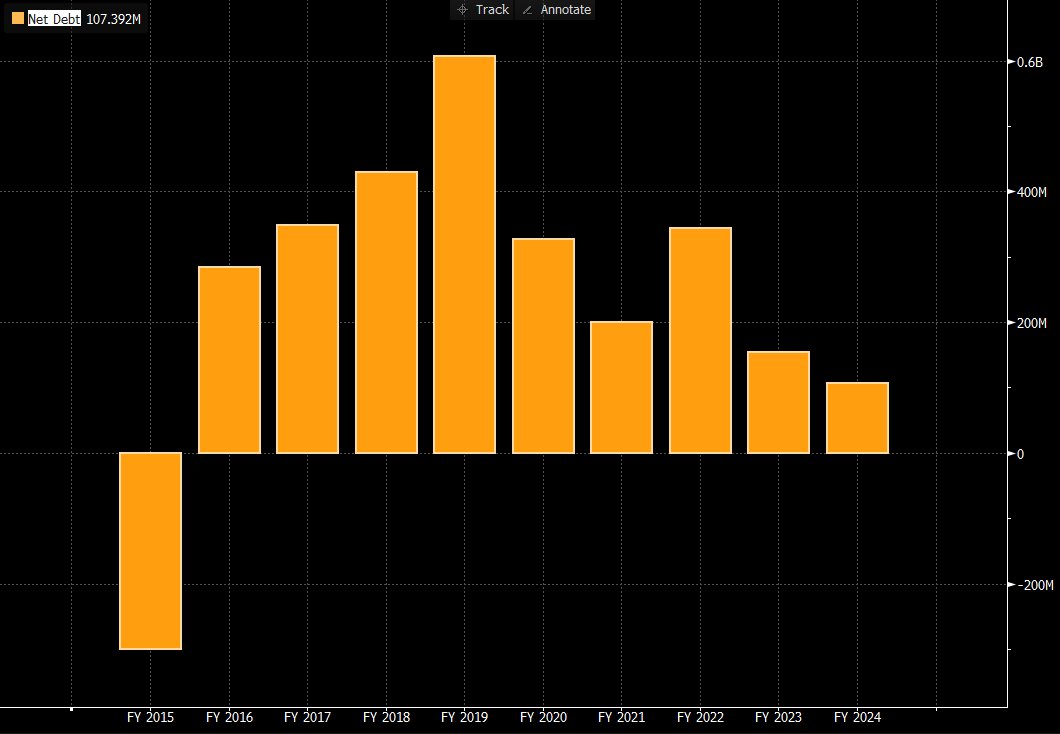

So many HK micro/small-cap run way too conservative balance sheets, MDG is a well-diversified business with low cyclicality in earnings. That means a more optimal balance sheet structure would be to run with some debt. And they did, they levered up after acquisitions in the US and Europe around the time of IPO. But since then, as MDG is such a cash-generative business, the debt has been paid off at a fast clip. So, for me as an investor, I was very keen to see the company “leverage up” again with further acquisitions.

Net Debt pre acquisition

As the purchase of Hexa Ceram was funded with available cash and minimal bank borrowings, with zero dilution for shareholders, this is very accretive to returns. I’m not sure if MDG will be able to find more bolts on like this, but it would be very positive if they could, preferably at reasonable multiples. Herein lies one of the problems: as MDG has such a low valuation, it gets harder to do slam-dunk acquisitions. They paid 8.25x EBITDA for Hexa Ceram. I would assume Hexa is of lower quality than the average of MDG, which is trading at 5-6x EBITDA. But in my view, if they integrate Hexa Ceram well and can find further acquisitions, at some point the market has to reward MDG with a higher multiple. Well, it’s listed in Hong Kong, so perhaps I should be careful with words as “has to”, forever shitco and all that.. :(

So what are my thoughts?

With the basics out of the way. Let’s start to address comments and discussions I had in the past:

New CEO

Mr Ngai has stepped down as CEO end of 2024, as the leadership has been shifting to the next generation of the family. A “bear argument” I heard from investors was that the top management was a bit too stacked, and too much money was spent on having them all on the payroll, so this is a small positive.

US market disappointing

The dental industry has been touted as a nice growth industry with boomers retiring and needing more dental services. Numbers like 5% CAGR have been thrown around for a long time. That might be true in some parts of the world like Europe. This has not materialized in the US in the past years, it’s rather been Covid hangover, which has been surprising to me and many others. Somehow, the US economy is running hot and stocks are taking all time highs, but the general broader consumer is hurting and can’t afford dental bills. Looking at data for the US, some tiny light can be seen in the tunnel with an uptick very recently:

One of the explanations I have been able to find for the weak US market, except the general economic situation of higher rates etc, is that dental policies are falling behind to cover the sharp inflation seen in the US:

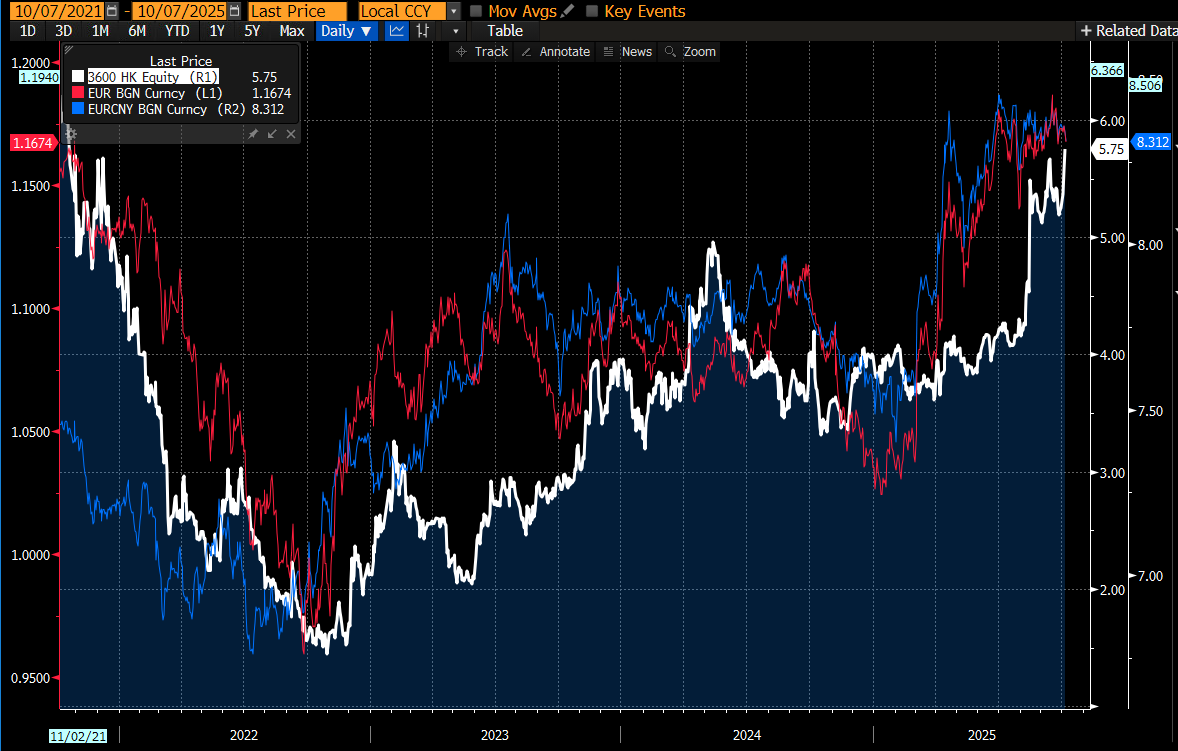

The wonderful Euro strength

The EUR appreciation is really a huge part of the good results and tailwind MDG is experiencing right now. It’s pretty simple, Europe is the largest region, items in Europe are priced in EUR, but MDG costs are in CNY and to some degree USD. This has meant that MDG for its European business has partly been at the mercy of the exchange rates. The FX has moved more than they have dared to re-price their products in EUR. This currency effect is larger on bottom-line margins than on top-line revenue. On different Y-axis scale in the chart below, is the MDG share price vs USDEUR and EURCNY:

After the significant USD strengthening in 2021-2022 and the collapse of the MDG stock, the currency movements have been a great predictor of future MDG share price. As we can see, the market is very bad at picking this up and only fully believes it when the actual numbers are released by MDG.

The recent EUR currency appreciation only happened in April 2025, which means the first half of 2025 results only include one quarter of the boost from currency. The next results will include the full boost from currency as long as the USD doesn’t significantly strengthen now in Q4 2025. That’s why I earlier said that I think the Bloomberg estimates for the second half of 2025 profits are very conservative. H1-2025 Net Income grew 33% YoY, and the Bloomberg estimate is for H2-2025 Net Income to grow the same 33% YoY. But as we can see from the currency graph, H2-2024 actually had a headwind from temporary USD strengthening.

So, adding up the two components, H2-2025 is the first half year with full EUR strengthening, instead of just one quarter, and the comparable in 2024 had weaker EUR in H2 than H1. For me this means that the 33% increase in Net Income YoY should not be enough in H2 2025. At the current share price of HK$5.75 that puts MDG on about 9.4x P/E multiple for 2025, I find that incredibly low.

So why is the valuation so low?

This brings me over to the final part, discussing threats and sharing that discussion I was referring to earlier, plus some comments from my dentist. Which ties into perhaps why the valuation is so low.

Before we jump into this, I do believe I overcomplicated things with the below discussions. I think the simple explanation is probably the best one. Modern Dental is undervalued as it’s a “strange” dental company listed on an exchange nobody cares about. It's fairly tightly held and semi-illiquid, so it’s not easy for funds to buy; no blocks are ever offered. It’s not included in HK Stock Connect either, so mainlanders can’t buy the shares; they have been the main buyers pushing up Hang Seng the past year. It’s a classical undiscovered stock with a large illiquidity premium.

In a nutshell, what are investors worried about?

Mostly one thing, technology, in terms of 3D printers and milling equipment, that can cut MDG out of the equation. Since day one, investing in MDG 7 years ago, I have heard this argument. It was also what the European investor wanted to have a call about and discuss. It was a valid concern 7 years, ago and it’s valid now, but MDG keeps performing. I try to constantly keep on top of this topic, but so far, I do not see any major shifts in this area, and that is why I’m bullish MDG. It’s still worthwhile to explain this worry in a bit more detail. Below is a fuller explanation. First, we have to take a step back to set the scene.

What role does a dental lab like MDG really fulfill?

MDG line of business is to produce different types of tooth replacements, some permanent, others removable. Examples would be crowns that go as a permanent cap on what is left of a tooth or an implant, others are removable, like “grandma’s fake teeth" she puts in a glass of water overnight, these are called dentures. There are also other products like bridges, which are a permanent cap over multiple teeth. There are different processes to create these products, with different pros & cons in terms of price, durability, comfort, and looks.

The process of creating these products has gone through quite a lot of innovation over the years, but there has always been some piece of artistry and expertise needed to get that final product to hit all of those requirements, especially comfort and looks. That’s why dental labs and dental lab technicians as a profession became a thing in the first place. It was such a separate and complex process to produce these custom-made products that no dentist wanted to deal with this inside their own clinic. It was better and more efficient for it to be handled by a separate technician who spent his whole career perfecting the production of such products. MDG, as the world’s largest dental lab, has perfected this process at scale to deliver high-quality products at a very competitive price point. But not everyone values a low price; some are willing to pay up for a better experience.

The dream of chairside instant products

The threat to MDG is based on a dream scenario for the dentist, that a customer at the dentist can have his crown, denture, or bridge immediately installed in the mouth in the same sitting as first-time visiting the dentist. Large and small start-up 3D printer companies are trying to solve for this dream scenario.

Do such machines exist that can offer such a service?

As I said, I have tried to keep my ear to the ground in terms of these types of products. There are multiple fairly well-funded early-stage 3D-printing companies that are trying to crack this nut and produce a machine that can do all the steps of what a dental technician does to produce, for example, dentures.

My friend (thanks Brandon) pointed me to one such start-up called: https://zylo3d.com/

This company claims to have solved what was long an argument for me around 3D-printing machines, that the finishing, curing, and color touches still needed to be done by a technician. Meaning previously 3D-printed products did 80-90% of the product, but the finishing touches still needed to be done by someone. That someone most often does not exist within a dental clinic, so buying such a machine, although not useless, often meant that the products were seen as temporaries for the dentists. For example, I have seen dentists on dental forums explain that they do use 3D-printers to print crowns, but as the quality is so sub-par that the printed crown would be used for that 1-2 week waiting time until the real crown, perhaps produced by MDG, would arrive.

This leads me to my largest personal skepticism around new products, the question of durability. A machine like Zylo3d is an unproven product; the product might look good and even feel good in the mouth, but the actual durability of everything we put in our mouth is still probably the most important point. Nobody wants to buy new dentures or a crown and be back in 1-2 years, with the product cracked, stained, color changes, or whatever other durability issue you can imagine. Perhaps Zylo3D has created the perfect product, but based on what I have seen from 3D printing technology, it is not so easy to make something so durable in a single machine process. That is why the main way to produce crowns is by milling out the crown from a solid block.

What do the dentists say?

Dentists acknowledge that chairside immediate access to the product would be great, but they see many hurdles to this. Some of them are from quality as discussed, but most point to the economic point of view, or personal preference on how to operate a dental clinic.

I haven’t been able to find any dentist I met in person who actually tried a Zylo3D machine or any other up-and-coming machine. This is actually the starting point of my argument, dentists in general are not interested in experimenting with new things, most of them want the tried and tested solutions they were trained on.

The dentist I met confirmed another aspect of MDG “moat” and that is the volume of crowns/dentures his clinic does per month is too low to warrant any such investment. He runs his own clinic, a single dentist. This is very typical around the world that dental clinics have 1-3 dentists. This is a key point for understanding where MDG can be most successful; they thrive in a fragmented market. Germany, a large market for MDG, has 99% small clinics (1-3 dentists). I think this also explains why MDG is struggling more in the US, as there has been much more VC-infused consolidation of the dental market. At large dental chains, it makes sense to go in-house and create your own dental lab.

Another good data point on how conservative and/or hesitant to spend money on equipment dentist are, would be how many of MDG cases/orders are received in digital format. The rest are mailed as physical clay molds to MDG in China. About 35-40% of cases are received with digital CAD scans from intraoral scanners. Using intraoral scanners instead of molds undoubtedly gives a better experience and results for the patients, still less than half of MDG customers use it, why? I put it down to several things:

Dentists’ habits and unwillingness to adopt new technology.

Cost, intra-oral scanners up until recently have been quite expensive; not all dental clinics operate with the latest shiny equipment, in fact, most don’t.

As mentioned, smaller clinics can’t share equipment costs in the same way, so small clinics will, in general, be late adopters of the latest tech.

Intraoral scanners have been around for a long time now, and MDG is strongly promoting their clients to switch to it, as the turnaround time, error rates will all be better. Still, more than half resist. It is not likely that these types of customers, that had many years to adopt intraoral scanners, will suddenly jump up and invest in a shiny new Zylo3D printing machine. For all the explanations above it doesn’t make sense.

I see the threat to MDG mainly is from the medium-sized dental clinics, which are currently MDG customers. They have the scale and probably the money to invest. Perhaps there is a middle segment like this where MDG long-term will lose a customer group they have today. Most people in the developed world are not worried about waiting 10 days for their crown; they are worried about the costs and that the outcome is good, and by sheer size and utilization of their machines, a mid-sized dental clinic can never match MDG cost efficiency. But probably for some clinics, the faster turnaround time will be more important, and the in-house-made products are “good enough”.

My conclusion

MDG does not need to win every dental clinic in the world to be successful; they only need to win the fragmented ones without the interest, resources, or volume of clients to make it rational to buy their own in-house machinery. So far, at least for the European and AU/NZ market, that seems to be the case. The US market it’s harder to tell how much it’s the bad Macro environment and how much it is that MDG struggles versus other lab alternatives, I’m guessing it’s a bit of both.

In the short term, the EUR strengthening is creating a massive tailwind to revenue and especially profit. Just like the Hexa Ceram acquisition, these are one-off improvements, but beneath that, MDG also keeps winning. The EUR is back trading in the same range as when I first invested in 2018, it’s a staggering difference in profit, up from below HK$100m to above HK$500m. Currently, I don’t see any reason why MDG should not keep winning in the long term also. Yes, a huge technological innovation or massive increase in consolidation of the dental industry are the two things that could reduce growth. This will not happen overnight, but it will be a slow-moving change.

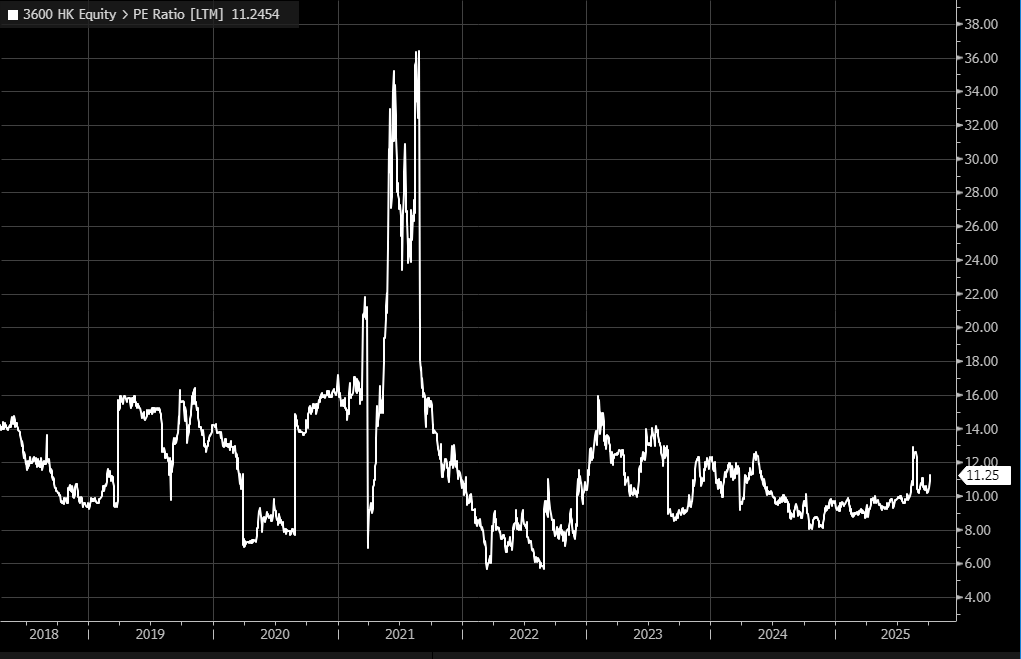

I leave you with a graph of Modern Dental’s 12-month trailing P/E ratio. Except for the hype period in 2021, the market has never believed in this company, pricing it as a business with huge risks of profits starting to fall. We now have the results for these 7 years, a 5x increase in profits. Where will we be in, say, another 3 years?

I hope these thoughts gave more clarity on MDG as an investment case, what the concerns are, and how I still see a bull case. Cheerio!